Holiday Planner

Holiday Planner Absence Management

Absence Management Performance Management

Performance Management Staff Management

Staff Management Document Management

Document Management Reporting

Reporting Health and Safety Management

Health and Safety Management Task Management

Task Management Security Centre

Security Centre Self Service

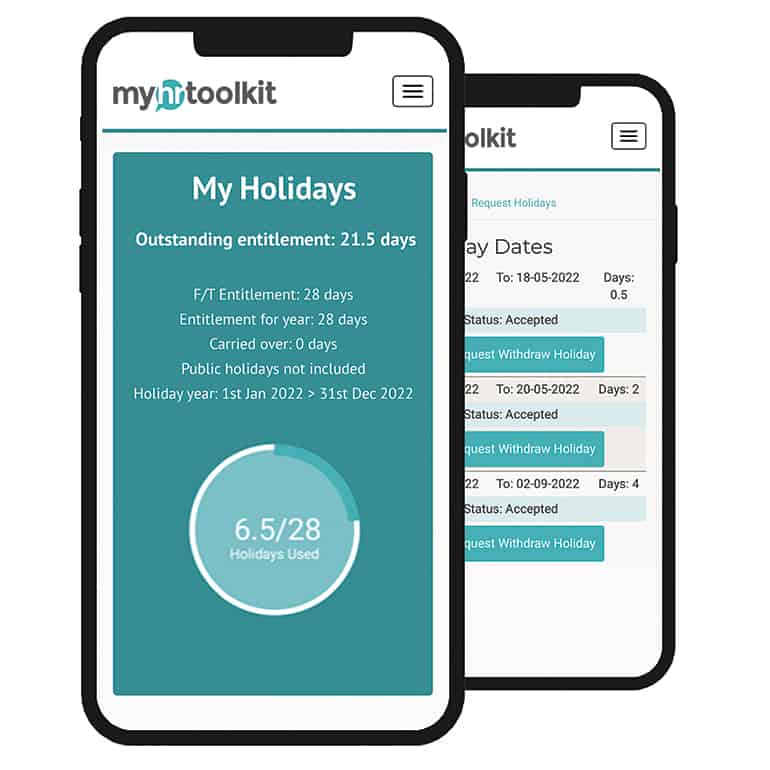

Self Service Mobile

Mobile

From April 2021, changes to IR35 (sometimes also known as off-payroll working rules) will mean that some small to medium-sized private businesses will be responsible for deciding on the employee status of self-employed or contracted workers who do work for them.

Up until this point, self-employed workers who are registered as part of a Limited Company were able to work for clients in such a way that they were not classified as employees of that company. This meant that the amount of tax they paid was different to the amount they would have paid - even, ostensibly, for doing the same work - if they had been registered as employees of that company.

Uncovering disguised employees

Self-employed contractors who register as part of a Limited Company are known as “disguised employees” since, while they work for employers, they are not officially recognised as such. This practice typically benefits both the self-employed contractor and the employer who they do work for, since each pays less tax than they would if the contractor had been registered as an employee with that company.

The changes to IR35 are set to remedy this by making private-sector employers with 50 or more employees responsible for deciding whether a self-employed contractor they employ is liable to be classed as an employee of the business.

Who’s responsible for deciding who counts as an employee?

So, when are employers responsible for deciding when a self-employed contractor they hire should be classed as an employee or not? This is where the legislation gets complicated. If businesses are treating contractors “as though they were an employee”, then contractors are liable for being classed as employees and paying the same amount of Income and National Insurance tax as regular employees. This will mean different things to different employers.

A good rule of thumb is whether the work done by a self-employed contractor could be readily performed by somebody else in their absence: if the answer is no, then they should probably be classified as an employee. See the UK government's website for more information on determining employment status.

Owner-managers of SMEs can minimise the risks that come with failing to comply with the new legislation by making self-employed contractors employees of their business. This reduces the chance of them becoming responsible for a self-employed contractor who is similar enough to an ordinary employee that they should be paying the same amount of tax as them. But it also costs employers, who will have to pay National Insurance contributions for these workers once they become enrolled on their payroll.

Related article: IR35 update: the importance of determining employment status

What about businesses with less than 50 employees?

Businesses that hire less than 50 employees will not be affected by the upcoming changes to IR35. For these companies, the responsibility for deciding whether the self-employed contractor should be classified as an employee will fall to the intermediary, which in this case is the contractor themselves or the Limited Company to which they are registered.

One caveat to this is businesses with under 50 employees that have an annual turnover of more than £10.2 million, or that have a balance sheet total of more than £5.1 million. These companies will be responsible for the employee status of self-employed contractors in the same way as larger businesses.

Employers should also note that the new changes to IR35 will apply to self-employed contractors entering into a contractual work agreement with an employer only after the date from which the new legislation comes into action. In the meantime, larger SMEs can begin preparing for the upcoming changes by accounting for how these changes might impact their bottom line.

Related articles

What is the difference between a worker and an employee?

Share this:

Written by Kate Taylor

Kate is a Content Marketing Executive for myhrtoolkit. She is interested in SaaS platforms, automation tools for making HR easier, and strategies for keeping employees engaged.